.jpg)

Magento vs PrestaShop in France: 1,349 vs 23,479 Stores — The Enterprise vs SME Divide

The comparison that actually matters

Most Magento vs PrestaShop comparisons treat them as interchangeable open-source alternatives. Both are self-hosted, PHP-based, and backed by corporate parents (Adobe and PrestaShop SA). Surface-level reviews compare admin panels and module ecosystems as if the two platforms compete for the same merchant. They do not.

Magento is the enterprise platform. Its 1,349 French stores generate an average of 1,990,650 EUR per year. Nearly a quarter of its merchants are ETI or GE — mid-cap and large enterprises. More than half are over 20 years old. PrestaShop is the SME workhorse. Its 23,479 stores average 238,266 EUR in annual revenue, 90% of its merchants are PMEs, and its median company age is 16 years. Same technology stack. Completely different market tiers.

This article uses lebot.in's June 2026 database of 155,000 SIREN-verified French e-commerce businesses to compare Magento and PrestaShop across traffic, revenue, industry, geography, and company structure. Every figure comes from that dataset. No feature comparisons, no pricing tables. Just the data.

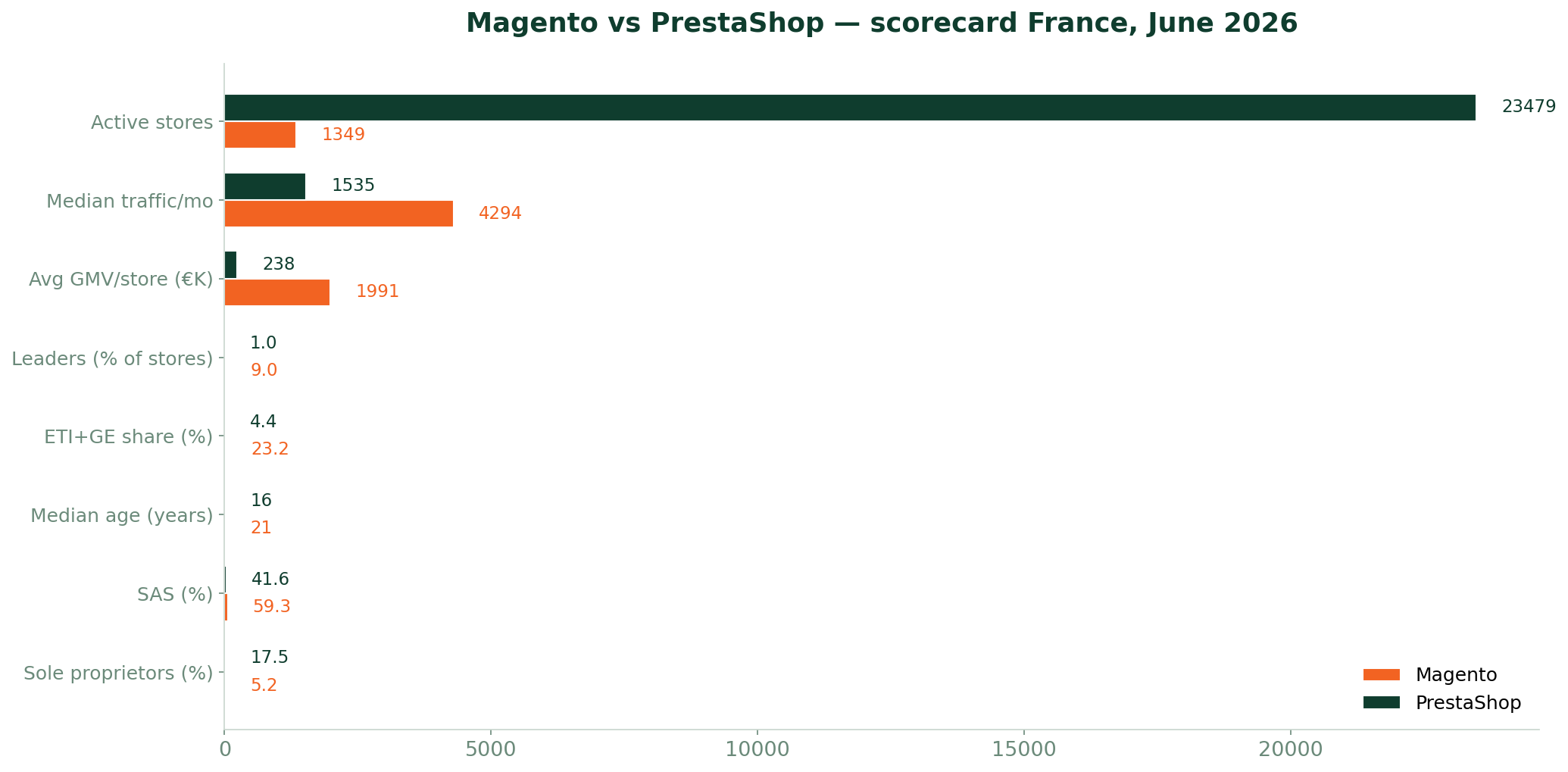

Scorecard: key metrics head to head

Here is the summary across eight dimensions that define each platform's position in France.

| Metric | Magento | PrestaShop |

|---|---|---|

| Active stores | 1,349 | 23,479 |

| Market share (France) | 1.0% | 18.2% |

| Median monthly traffic | 4,294 | 1,535 |

| Total estimated GMV | 2.69B EUR | 5.59B EUR |

| Average GMV per store | 1,990,650 EUR | 238,266 EUR |

| Stores with >100K visits/mo | 121 (9.0%) | 239 (1.0%) |

| Median company age | 21 years | 16 years |

| ETI + GE share | 23.2% | 4.4% |

The scorecard makes the structural difference unmistakable. PrestaShop has 17 times more stores and twice the total GMV. But Magento's average GMV per store is 8.4 times higher. Nine percent of Magento stores qualify as Leaders with over 100,000 monthly visits — nine times the proportion on PrestaShop. And nearly a quarter of Magento merchants are mid-cap or large enterprises, compared to fewer than one in twenty on PrestaShop.

These are not competing platforms. They are adjacent layers of the same market, separated by an order of magnitude in store economics.

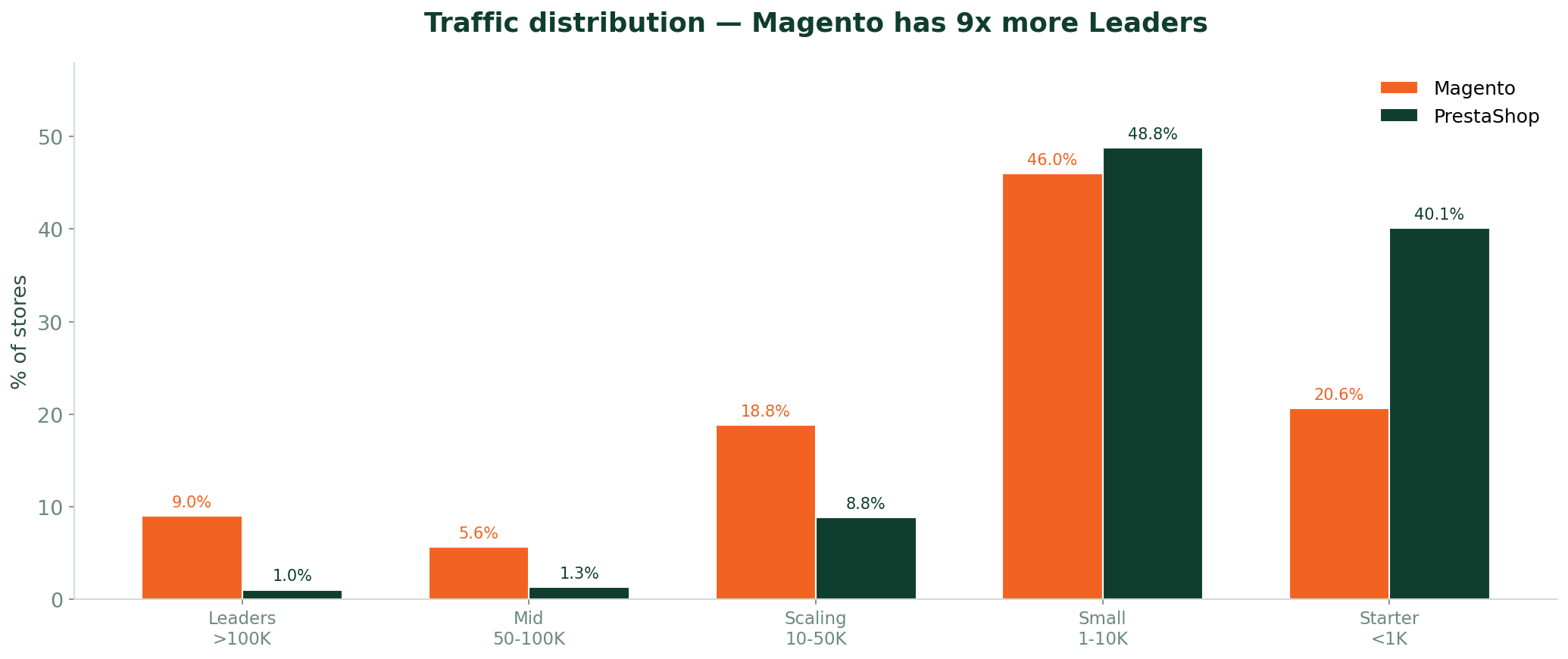

Traffic and performance distribution

Store count measures presence. Traffic distribution reveals performance.

Magento traffic segments

| Segment | Monthly visits | Share of stores |

|---|---|---|

| Starters | <1,000 | 20.6% |

| Small | 1,000--10,000 | 46.0% |

| Scaling | 10,000--40,000 | 18.8% |

| Mid-market | 40,000--100,000 | 5.6% |

| Leaders | >100,000 | 9.0% |

PrestaShop traffic segments

| Segment | Monthly visits | Share of stores |

|---|---|---|

| Starters | <1,000 | 40.1% |

| Small | 1,000--10,000 | 48.8% |

| Scaling | 10,000--40,000 | 8.8% |

| Mid-market | 40,000--100,000 | 1.3% |

| Leaders | >100,000 | 1.0% |

Magento's traffic distribution is the healthiest of any major platform in France. Only 20.6% of its stores are Starters — half the rate of PrestaShop (40.1%) and a fraction of Shopify (64.2%) or WooCommerce (69.7%).

The gap widens at every tier above 10,000 visits. Scaling (10K--40K): 18.8% vs 8.8%. Mid-market (40K--100K): 5.6% vs 1.3%. Leaders (>100K): 9.0% vs 1.0%. In absolute numbers, Magento's 121 Leaders trail PrestaShop's 239. But 121 out of 1,349 total stores is a concentration rate no other major platform matches. Magento does not have many stores in France. The ones it has are disproportionately large.

Industry verticals

Both platforms are dominated by retail commerce. The sector composition is more similar than different, but the nuances are revealing.

Magento: top sectors by NAF code classification

| Sector | Share of stores |

|---|---|

| Commerce (retail/wholesale) | 67.6% |

| Manufacturing | 14.0% |

| IT and communications | 5.7% |

| Professional services | 3.0% |

PrestaShop: top sectors by NAF code classification

| Sector | Share of stores |

|---|---|

| Commerce (retail/wholesale) | 63.6% |

| Manufacturing | 14.7% |

| IT and communications | 5.0% |

| Professional services | 3.7% |

| Agriculture | 2.4% |

Magento is slightly more retail-concentrated (67.6% Commerce vs 63.6%). Manufacturing and IT are nearly identical across both platforms. The most distinctive gap is Agriculture: PrestaShop holds 2.4% of its base in agricultural businesses — producers, cooperatives, terroir operations — a segment absent from Magento's top sectors. Magento's infrastructure costs put it out of reach for most small agricultural businesses.

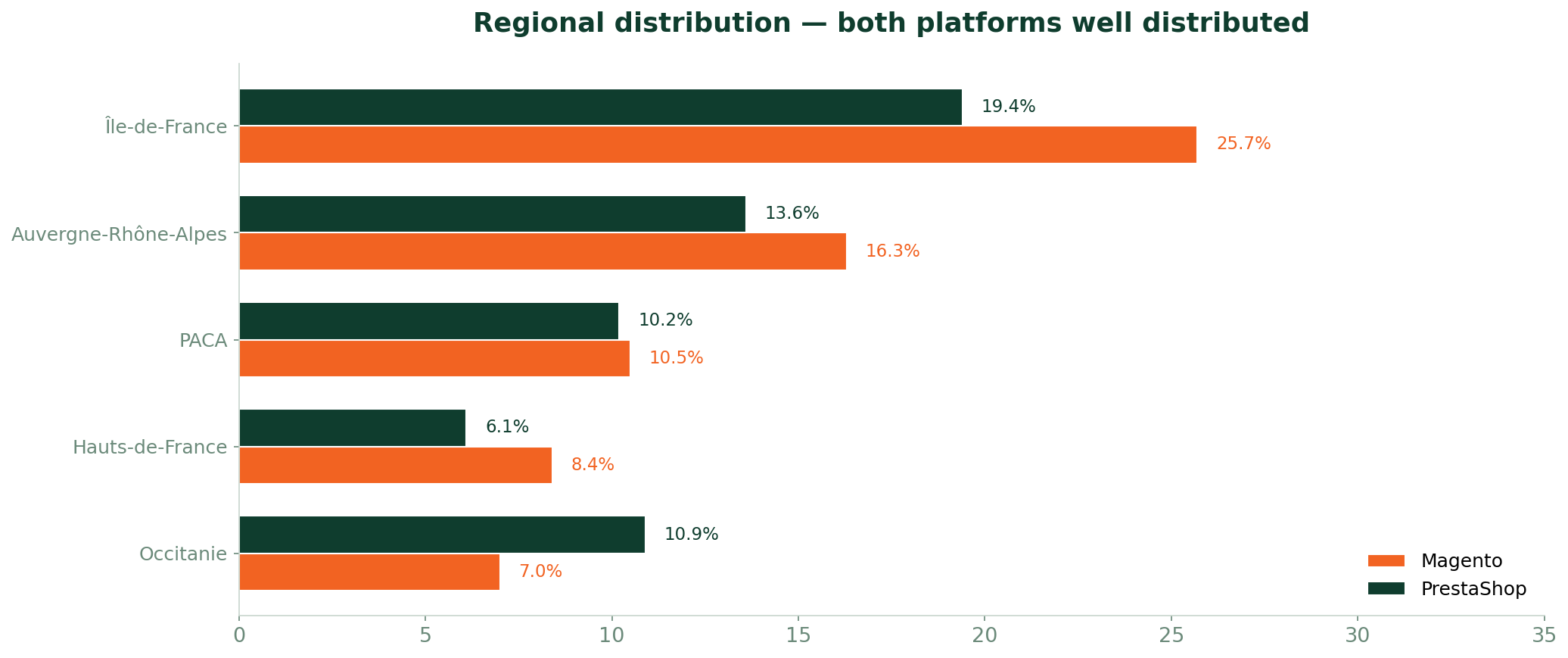

Geography: where each platform sits

Magento: regional distribution

| Region | Share of stores |

|---|---|

| Ile-de-France | 25.7% |

| Auvergne-Rhone-Alpes | 16.3% |

| Provence-Alpes-Cote d'Azur | 10.5% |

| Hauts-de-France | 8.4% |

PrestaShop: regional distribution

| Region | Share of stores |

|---|---|

| Ile-de-France | 19.4% |

| Auvergne-Rhone-Alpes | 13.6% |

| Occitanie | 10.9% |

| Provence-Alpes-Cote d'Azur | 10.2% |

Magento is more Paris-centric than PrestaShop (25.7% vs 19.4% in Ile-de-France) but considerably less so than Shopify (37.9%). Enterprise retailers cluster in the capital where corporate headquarters and specialized development agencies concentrate. Magento also has strong representation in Auvergne-Rhone-Alpes (16.3%), reflecting large manufacturing and retail operations in the Lyon-Grenoble corridor.

Hauts-de-France appears in Magento's top four at 8.4%, a region that does not feature prominently for other platforms — likely reflecting the concentration of large retail chains historically based in the Lille-Roubaix-Tourcoing area. PrestaShop shows strength in Occitanie (10.9%), a region driven by smaller merchants and local agencies.

Company profile: who uses each platform

The structural characteristics of merchants confirm the enterprise-versus-SME divide.

Company size

| Size category | Magento | PrestaShop |

|---|---|---|

| PME (SME) | 73.5% | 89.6% |

| ETI (mid-cap) | 19.3% | 4.0% |

| GE (large enterprise) | 3.9% | 0.4% |

Nearly one in five Magento stores belongs to an ETI. Large enterprises represent 3.9% of the base, ten times PrestaShop's 0.4%. Combined, 23.2% of Magento merchants are ETI or GE versus 4.4% on PrestaShop.

This metric alone explains why Magento persists in France despite a tiny store count. It holds the segment where enterprise requirements — complex catalogs, multi-store architecture, deep ERP integration — justify its higher total cost of ownership.

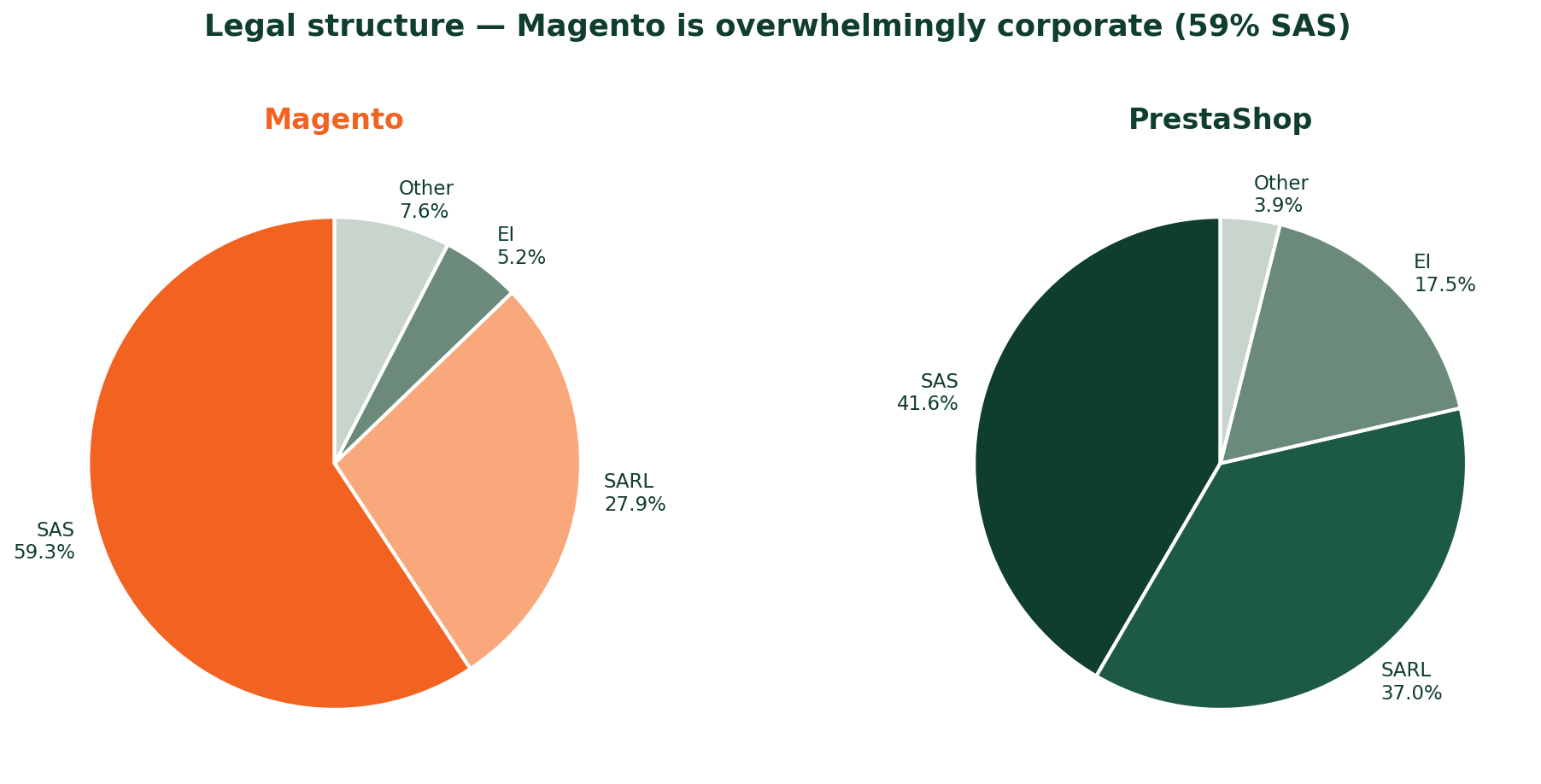

Legal form

| Legal structure | Magento | PrestaShop |

|---|---|---|

| SAS (simplified joint-stock) | 59.3% | 41.6% |

| SARL (limited liability) | 27.9% | 37.0% |

| EI (sole proprietor) | 5.2% | 17.5% |

Magento's legal profile is overwhelmingly corporate. Nearly six in ten stores are SAS companies — the preferred structure for businesses with external investors and significant capitalization. Only 5.2% are sole proprietors, compared to 17.5% on PrestaShop. This is not a platform where a solo entrepreneur installs a module and starts selling. It is a platform where a procurement committee selects an agency and budgets a six-figure implementation.

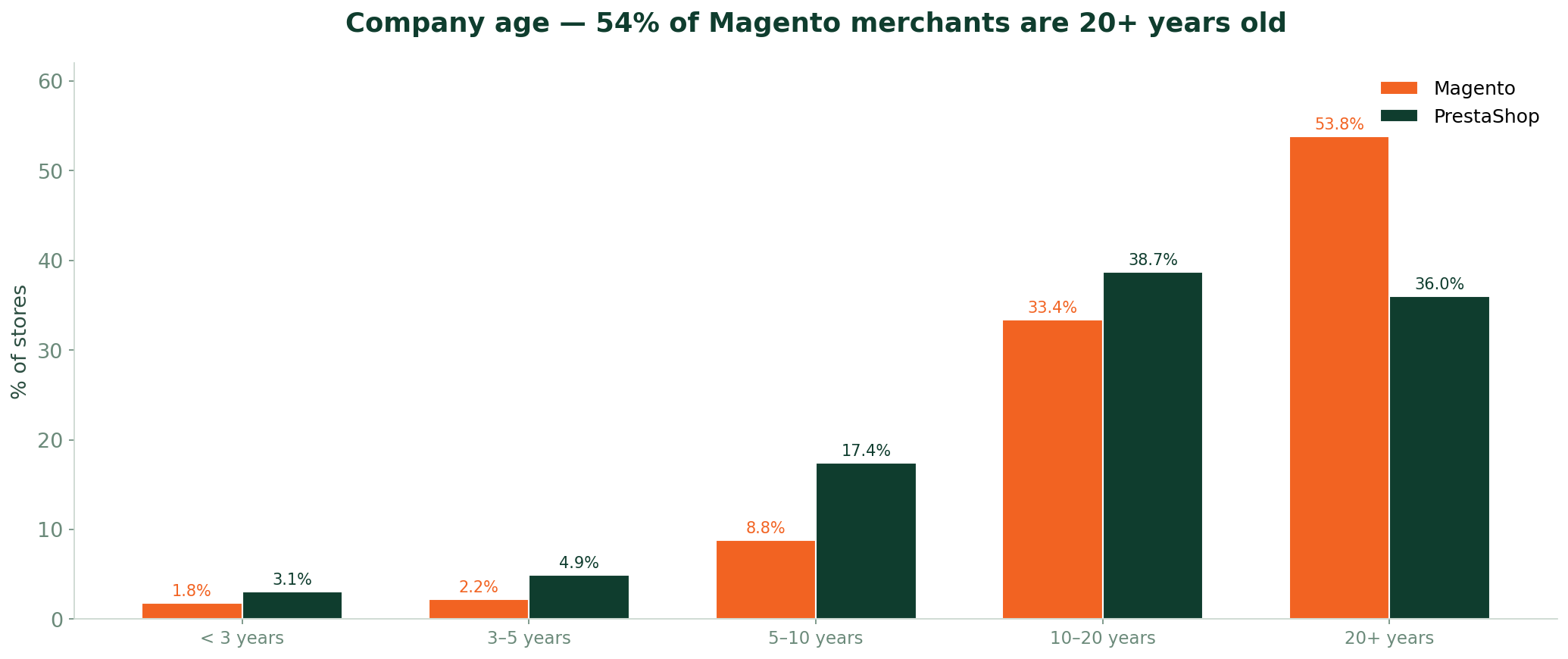

Company age

| Age bracket | Magento | PrestaShop |

|---|---|---|

| Less than 3 years | 1.8% | 3.1% |

| 3 to 5 years | 2.2% | 4.9% |

| 5 to 10 years | 8.8% | 17.4% |

| 10 to 20 years | 33.4% | 38.7% |

| More than 20 years | 53.8% | 36.0% |

More than half of all Magento merchants have been in business for over 20 years. Only 1.8% are less than 3 years old. Magento is not attracting new entrants. It is holding established retailers who adopted the platform during the 2010--2015 era and have not migrated away. PrestaShop is also mature but more balanced, still attracting some new businesses (8.0% under 5 years) with a thicker 5-to-20-year band.

Domain extension (TLD)

| TLD | Magento | PrestaShop |

|---|---|---|

| .com | 49.7% | 46.5% |

| .fr | 44.4% | 49.3% |

Magento merchants lean slightly toward .com (49.7% vs 46.5%), consistent with the international orientation of enterprise retailers who often serve multiple European markets from a single French entity. PrestaShop merchants prefer .fr (49.3%), reflecting their focus on the domestic French market. The difference is modest but directionally consistent with the enterprise-versus-SME narrative.

GMV and revenue distribution

Revenue distribution is where the 8.4x gap in average GMV per store comes into sharp focus.

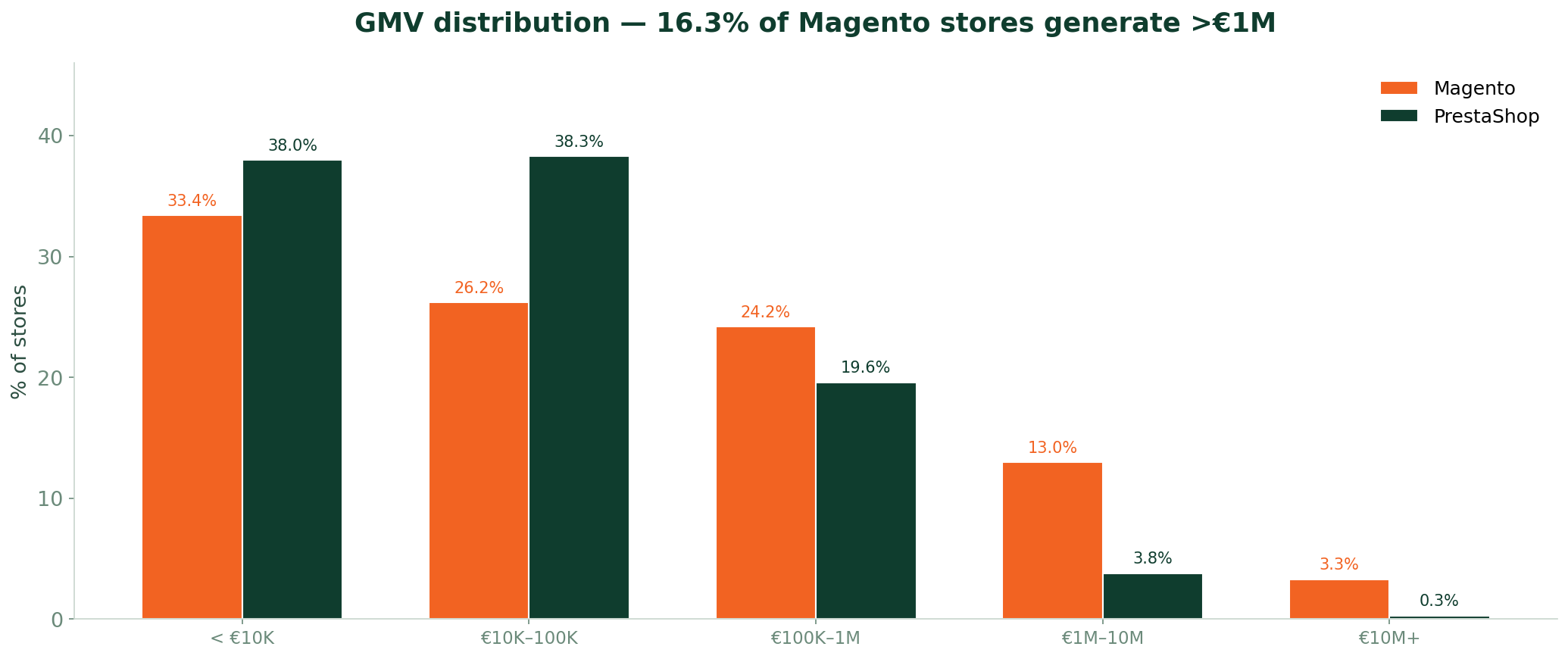

GMV brackets

| Annual GMV | Magento | PrestaShop |

|---|---|---|

| Less than 10K EUR | 33.4% | 38.0% |

| 10K--100K EUR | 26.2% | 38.3% |

| 100K--1M EUR | 24.2% | 19.6% |

| 1M--10M EUR | 13.0% | 3.8% |

| More than 10M EUR | 3.3% | 0.3% |

The bottom of the table is closer than expected: 33.4% of Magento stores generate less than 10,000 EUR per year, compared to 38.0% on PrestaShop. Even Magento has a long tail of low-revenue stores.

The divergence begins above 100K EUR and accelerates above 1 million. Fully 13.0% of Magento stores generate between 1M and 10M EUR annually versus 3.8% on PrestaShop. At the summit, 3.3% exceed 10M EUR versus 0.3%. In total, 16.3% of Magento stores generate more than 1 million EUR per year. On PrestaShop, 4.1% cross that threshold.

Top Magento stores in France

The names behind Magento's top tier illustrate the platform's positioning. Bouygues Telecom runs on Magento with 16.2 million monthly visits and 619 million EUR in annual GMV. Electro Depot generates 5.8 million visits and 188 million EUR. Promesse de Fleurs draws 1.9 million visits and 108 million EUR. Mondial Tissus and Adopt round out the top five with traffic in the 1.1 million range.

These are category leaders with complex operations — multi-warehouse logistics, product configurators, B2B and B2C channels, and deep ERP integration. This is the market segment Magento was built for.

Verdict: which platform for which use case

This is not a competition. The right choice is determined by where you sit on the enterprise spectrum.

Choose Magento if:

You are an ETI or large enterprise with a dedicated technology team. You need deep ERP integration with SAP, Oracle, or custom systems. Your catalog is complex — configurable products, B2B pricing tiers, multi-store or multi-country architecture. You have the budget for a six-figure implementation. Your annual online revenue exceeds 1 million EUR.

Choose PrestaShop if:

You are a PME with a standard product catalog. You are cost-sensitive and value access to the French PrestaShop ecosystem — local agencies, French-language documentation, and a module marketplace tailored to French tax, shipping, and payment requirements. You work with a local web agency rather than an in-house development team.

For B2B teams selling to merchants:

Magento is the ultra-high-value, low-volume play: 1,349 companies averaging nearly 2 million EUR in annual GMV. The list is small enough for a named-account strategy. PrestaShop is the volume play: 23,479 targets, mostly PMEs, with lower revenue per account but far more pipeline breadth. A Magento-focused strategy requires enterprise sales. A PrestaShop-focused strategy requires scalable outreach.

Frequently Asked Questions

Is Magento bigger than PrestaShop in France?

By store count, PrestaShop is overwhelmingly larger: 23,479 active stores versus 1,349 for Magento, representing 18.2% and 1.0% of the French market respectively. PrestaShop also leads in total GMV (5.59 billion EUR vs 2.69 billion EUR). However, the average Magento store generates 8.4 times more revenue than the average PrestaShop store (1,990,650 EUR vs 238,266 EUR). Magento is smaller by every volume metric but dramatically larger on a per-store basis.

Which generates more revenue --- Magento or PrestaShop stores?

Magento stores generate far more revenue on average: 1,990,650 EUR in estimated annual GMV versus 238,266 EUR on PrestaShop. Median monthly traffic tells the same story: 4,294 visits versus 1,535. The top Magento stores — Bouygues Telecom, Electro Depot, Promesse de Fleurs — generate hundreds of millions annually. PrestaShop's total platform GMV is higher only because it has 17 times more stores.

What size company uses Magento vs PrestaShop?

Magento skews heavily toward larger companies. Nearly a quarter of its merchants (23.2%) are ETI or GE — mid-cap and large enterprises. On PrestaShop, that share is 4.4%. Magento merchants are predominantly SAS companies (59.3%), with only 5.2% sole proprietors. PrestaShop is dominated by PMEs (89.6%), with 17.5% sole proprietors and 37.0% SARLs. The median Magento company has been in business for 21 years versus 16 years for PrestaShop.

Is Magento dying in France?

Magento is not growing in France. Only 1.8% of its merchants are less than 3 years old, and new entrants overwhelmingly choose Shopify, PrestaShop, or WooCommerce. But the platform is far from dying. Its 1,349 stores include some of the largest French online retailers, collectively generating 2.69 billion EUR annually. Magento is better described as entrenched — a small, deeply committed installed base with high switching costs and no clear migration path that preserves their customization.

What are the biggest Magento stores in France?

The largest by traffic is Bouygues Telecom (16.2 million monthly visits, 619 million EUR GMV), followed by Electro Depot (5.8 million visits, 188 million EUR), Promesse de Fleurs (1.9 million visits, 108 million EUR), Mondial Tissus (1.1 million visits, 13 million EUR), and Adopt (1.1 million visits, 31 million EUR). All are established French retail brands with complex operational requirements.

Should I migrate from PrestaShop to Magento?

Migration only makes sense if your business has outgrown PrestaShop's capabilities and you can justify six-figure implementation budgets and scarce Magento developer talent. The move is justified if you need multi-store architecture, complex B2B pricing, deep ERP integration, or catalogs with thousands of configurable items. If your annual revenue is below 1 million EUR and your catalog is standard, PrestaShop remains more cost-effective. Most businesses migrating away from PrestaShop today move to Shopify rather than Magento.

Methodology

All data in this article comes from lebot.in's June 2026 database of 155,000 French e-commerce businesses. Each store is matched to a SIREN — the nine-digit French legal entity registration number assigned by INSEE. Platform detection uses technology fingerprinting across live websites. Traffic estimates are sourced from SimilarWeb data. GMV estimates are modeled from traffic volumes, industry-specific conversion rates, and average order values. Company metadata (legal form, age, size classification, NAF sector code, region) is sourced from official French business registries. For a full description of the database and its coverage, see the June 2026 database overview.

Further Reading

- [French E-Commerce Database: 155,000 Online Stores Mapped](https://www.lebot.in/en/insights/french-ecommerce-database-june-2026) --- the full June 2026 database overview with platform, region, and legal entity breakdowns.

- [PrestaShop vs Shopify in France: 23,479 vs 28,583 Stores Compared by Data](https://www.lebot.in/en/insights/battlecard-prestashop-vs-shopify-france) --- head-to-head data comparison of PrestaShop and Shopify in the French market.

- [Shopify vs WooCommerce in France: 28,583 vs 60,563 Stores](https://www.lebot.in/en/insights/battlecard-shopify-vs-woocommerce-france) --- data-driven comparison of Shopify and WooCommerce across the French e-commerce landscape.

- [StoreLeads Alternative: Benchmarking Shopify France](https://www.lebot.in/en/insights/storeleads-alternative-benchmark-shopify-france) --- how lebot.in's database compares to StoreLeads for Shopify store intelligence in France.

Your prospects are in our database. Let's talk.

Our team is available to present the solution and help you build your first e-commerce prospect segment.

Book a meeting →